Nouriel Roubini made various claims and predictions today in an interview on CNBC:

- QE2 will be followed by several more rounds, up to QE4 or QE5. (This prediction matches the TransEconomics view that, if necessary, the Fed will end up more than doubling the size of its balance sheet to to $5 trillion.)

- David Cameron and Mervyn King in the UK have an implicit agreement whereby the Bank of England will offset Treasury tightening with monetary loosening. The monetary loosening will take the form of QE2 a l'anglaise and will start as soon as fiscal pain (rock throwing) becomes unbearably intense.

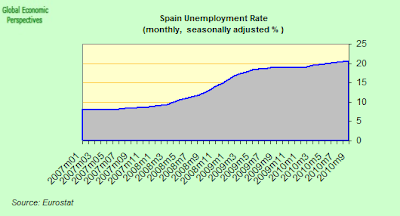

- Given falling output in the European Union periphery and deflationary fiscal policy in Europe, the European Central Bank's current resistance to more quantitative easing is "not productive".

- We will probably see private orderly restructuring of sovereign debt in Greece first, then Portugal, and finally Ireland.

- Restructuring can take the form of exchange deals: sovereigns exchange outstanding bonds for some other assets. This is worked out with bondholders: no supranational entity (EU or IMF) need be involved.

- QE2 in the USA coupled with insufficiently fast appreciation of the Chinese yuan can lead to new or enlarged existing asset bubbles in China, even if China tightens credit and money.

Hoy en entrevista en CNBC, Nouriel Roubini predijo y afirmó:

- Después de esta ronda de estímulo cuantitativo (QE2) nos esperan más rondas, hasta QE4 or QE5. (Este punto es consistente con nuestra opinión en TransEconomics de que, si es neceario, la Fed más que duplicará el tamaño de su balance, hasta $5 billones.)

- David Cameron y Mervyn King en el Reino Unido tienen un acuerdo implícito según el cual Banco de Inglaterra contrarrrestará la política restrictiva del Tesoro con estímulo cuantitativo. El estímulo tomará la forma de un QE2 a la inglesa y comenzará tan pronto el dolor fiscal se torne insportable (los disturbios aumenten).

- Dada la contracción económica en la periferia de la Zona del Euro y la restricción fiscal en Europa, la resistencia del BCE a aplicar más estímulo cuantitativo (que el BCE llama "relajamiento crediticio") "no es productiva".

- Probablemente veremos una ordenada reestructuración privada de deuda en Grecia, primero, luego Portugal e Irlanda.

- Estos soberanos pueden canjear bonos por algún otro activo. El trato puede hacerse con inversionistas privados, sin que intervenga ninguna institución subpranacional del tipo FMI o Unión Europea.

- Aunque China restrinja el crédito y el dinero, QE2 en EEUU y demasiado lenta depreciación del yuan pueden provocar que en China la inflación se acelere y las burbujas financieras se multipliquen y se expandan.